How Much of a $25K, $50K, or $100K Settlement Do You Keep in Illinois?

Short answer: you do not keep the full settlement. In an Illinois car accident case, the gross settlement is usually reduced by attorney fees, case costs, and medical bills or liens before the final check goes out. That is why people asking how much their Illinois car accident case is worth should also ask what the net payout may actually look like.

How settlement math works in an Illinois car accident case

The math usually looks like this:

Gross settlement − attorney fee − case costs − medical liens / unpaid medical balances = your net check

That sounds simple, but the real numbers can change fast depending on whether the case settles early, whether a lawsuit has to be filed, and whether hospitals, doctors, or therapists have valid liens against the recovery.

The amount you keep from a settlement depends on more than the headline number. A fair settlement also has to account for the injury’s impact on your life, including medical treatment, lost income, liens, fees, expenses, and pain and suffering after a car accident.

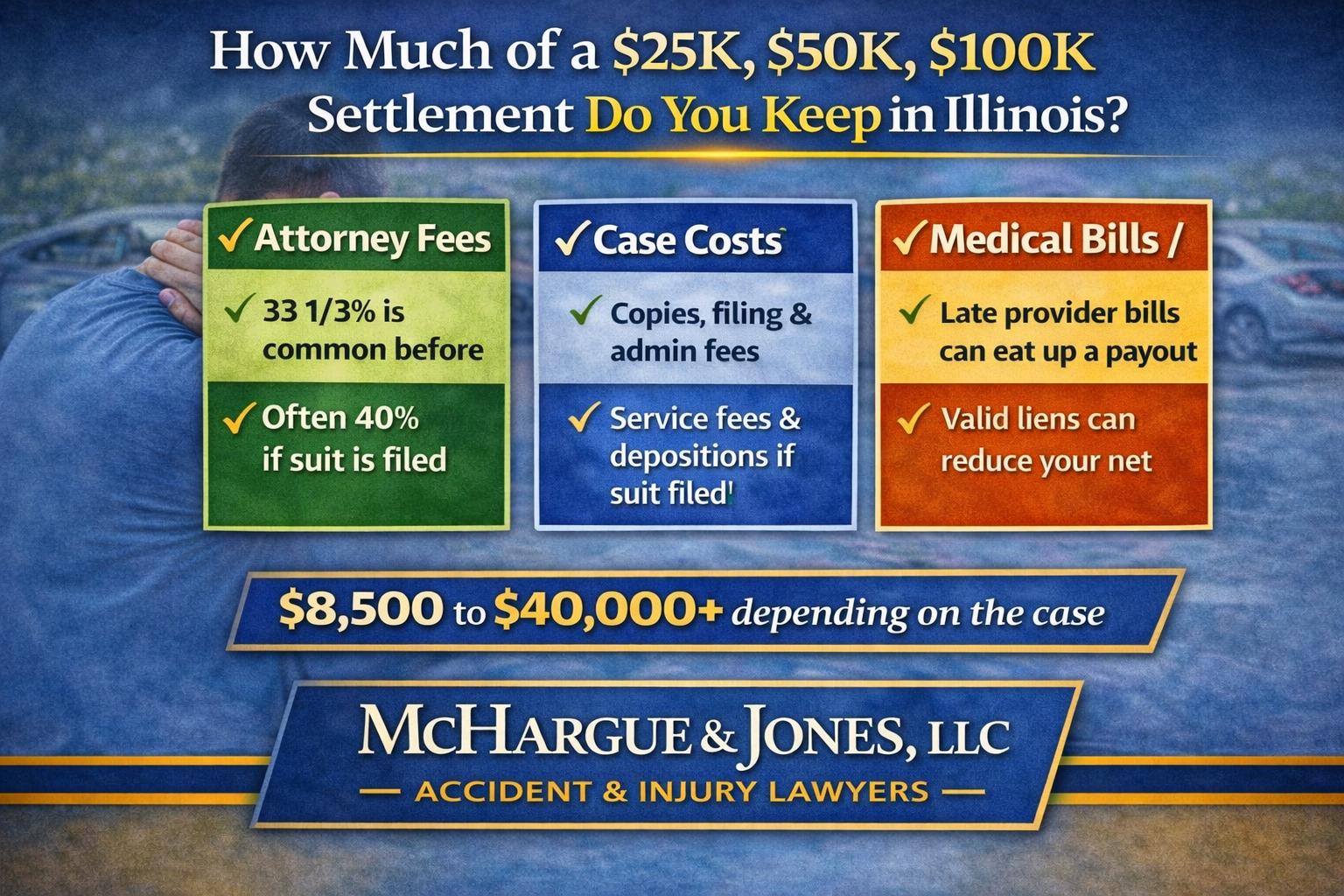

Attorney fees are often one-third before suit, but can jump to 40% after filing

In many Illinois injury cases, the contingency fee is commonly around 33 1/3% if the claim settles before a lawsuit is filed. A lot of Illinois retainer agreements then move to 40% if suit is filed or the case proceeds further into litigation. That does not happen in every case, and the actual percentage depends on the contract you signed, but it is a common fee structure in Illinois personal injury practice.

This matters because filing suit can change two numbers at the same time:

- the fee percentage may increase, and

- the case costs often increase too because litigation is more expensive.

For a broader explanation of contingency fees, see how much a car accident lawyer costs in Illinois.

Case costs are separate from the fee

Even when the lawyer works on contingency, most cases still have costs. Before suit, these may be modest and include record charges, police reports, postage, and filing-related admin expenses. After a lawsuit is filed, costs can rise because of court filing fees, service fees, depositions, subpoenas, expert review, and similar litigation expenses.

Will the Insurance Company Offer a Settlement—and Do You Need a Lawyer Before Accepting?

Before you can calculate how much of a car accident settlement you will actually keep, there has to be a settlement offer in the first place. Insurance companies do not automatically offer fair compensation just because a crash happened. The adjuster usually wants to investigate fault, review the medical records, confirm available insurance coverage, and decide what they believe the claim is worth.

That is why some Illinois car accident claims receive an offer quickly, while others stall for months. A property-damage-only claim may move faster. An injury claim usually takes longer because the insurance company wants to know the full medical picture: what treatment you needed, whether you missed work, whether you have ongoing pain, whether you may need future care, and whether the crash actually caused the injuries being claimed.

Even when the insurance company does make an offer, the first number is not always the number you should accept. A settlement offer is a gross number. It does not tell you what you will keep after attorney fees, case expenses, medical bills, liens, health insurance reimbursement claims, or unpaid provider balances are resolved.

This is where having a lawyer can matter. A car accident lawyer can help evaluate whether the offer is fair, whether the policy limits are affecting the number, whether medical liens can be reduced, whether future treatment has been considered, and whether filing suit may increase the value enough to justify the higher fee and litigation costs.

It is especially important to be careful before signing a release. Once you accept a settlement and sign a release, you usually give up the right to ask for more money later—even if your pain gets worse, your medical bills increase, or you later learn that the settlement did not account for all liens and deductions.

If you are still waiting for an offer, received a low offer, or are not sure whether the insurance company is treating your claim fairly, read our guide on whether insurance will offer a settlement after a car accident in Illinois. Then use the settlement math below to understand what that offer may actually mean for your final net check.

What Our Clients Say

Real Google reviews from injured workers we’ve helped across Illinois.

Medical liens can have a major effect on what you actually keep

The biggest surprise for many people is not the lawyer fee. It is the medical lien side of the case. If you treated on a lien, still owe providers, or receive formal lien notices, those claims may have to be dealt with before the settlement is disbursed.

How the Illinois Health Care Services Lien Act can change the payout math

Illinois has a lien statute that can matter a lot in personal injury cases. Under the Illinois Health Care Services Lien Act, qualifying health care professionals and health care providers can assert liens against a settlement, verdict, or award. But the Act also places limits on how much those liens can take from the recovery.

In general, qualifying health-care-services liens under the Act cannot exceed 40% of the recovery in the aggregate. If the total qualifying liens meet or exceed that threshold, the statute generally allocates up to 20% to health care professionals and up to 20% to health care providers, subject to the Act’s additional rules. That can protect some of the client’s net recovery in smaller and mid-sized cases.

That said, the lien act does not mean every medical claim disappears. Final distribution can still depend on the type of bill, whether the lien was properly perfected, whether reductions are negotiated, and whether there are other reimbursement or subrogation issues in play. In other words, the settlement number alone does not tell you what will actually land in your pocket.

How much of a $25,000 settlement do you get in Illinois?

Here is a realistic example using common Illinois fee structures. These are sample numbers, not guarantees.

| Scenario | Gross Settlement | Attorney Fee | Case Costs | Medical Bills / Liens | Estimated Net |

|---|---|---|---|---|---|

| Pre-suit settlement at 33 1/3% | $25,000 | $8,333 | $500 | $5,000 | $11,167 |

| After suit filed at 40% | $25,000 | $10,000 | $1,500 | $5,000 | $8,500 |

On a $25,000 case, a lawsuit can make a noticeable difference in the final number because both the fee percentage and the costs may go up. And if the $25,000 recovery is also the other driver’s policy limit, the settlement may reflect the coverage cap, not the true value of the injury claim. That is where an underinsured motorist claim in Illinois can become important.

How much of a $50,000 settlement do you get in Illinois?

| Scenario | Gross Settlement | Attorney Fee | Case Costs | Medical Bills / Liens | Estimated Net |

|---|---|---|---|---|---|

| Pre-suit settlement at 33 1/3% | $50,000 | $16,667 | $750 | $12,500 | $20,083 |

| After suit filed at 40% | $50,000 | $20,000 | $2,500 | $12,500 | $15,000 |

A $50,000 settlement often leaves more room to resolve medical liens and still produce a meaningful net check, but the final number still depends heavily on treatment volume and whether the bills were reduced. If the gross settlement looks strong but the medical side is heavy, the client’s actual take-home can still be lower than expected.

How much of a $100,000 settlement do you get in Illinois?

| Scenario | Gross Settlement | Attorney Fee | Case Costs | Medical Bills / Liens | Estimated Net |

|---|---|---|---|---|---|

| Pre-suit settlement at 33 1/3% | $100,000 | $33,333 | $1,500 | $25,000 | $40,167 |

| After suit filed at 40% | $100,000 | $40,000 | $5,000 | $25,000 | $30,000 |

On a six-figure settlement, the fee increase from 33 1/3% to 40% becomes even more visible. That does not mean filing suit is a mistake. Sometimes filing suit is exactly what is needed to move the case forward or force a fairer result. It just means clients should understand how the fee and cost structure may change once litigation begins.

Why two people with the same settlement can walk away with very different net checks

Two people can both settle for $50,000 and still receive very different amounts because the deductions may be different. One may have low treatment costs and no major liens. Another may have a hospital lien, physical therapy balances, or case costs that rose after suit was filed. Same gross settlement, very different net outcome.

Can the lawyer charge extra for reducing a lien?

Usually not as a separate add-on fee beyond the contingency agreement. In Illinois, bar ethics guidance says a lawyer generally cannot take an additional legal fee on top of the agreed contingency percentage simply for negotiating a lien reduction. That matters because clients should understand the distribution sheet and make sure the deductions match the actual fee agreement and actual case expenses.

Why the Illinois lien act matters most in smaller settlement cases

The lien act can make a major difference in smaller cases where medical providers would otherwise consume most of the recovery. A $25,000 settlement with hospital and provider claims can look bleak at first, but the Health Care Services Lien Act may reduce the amount qualifying lienholders can take. That can preserve more of the client’s net than people expect.

Why policy limits still matter when you calculate what you keep

Sometimes a $25,000 or $50,000 settlement is not really a reflection of the injury value at all. It is the available insurance. If the at-fault driver was uninsured or underinsured, the next step may be an uninsured motorist claim in Illinois or an underinsured motorist claim in Illinois. That is why payout math and insurance analysis go together.

FAQ: How much of a settlement do you actually keep in Illinois?

How much of a $25,000 settlement do I get after attorney fees and medical bills?

It depends on the fee agreement, case costs, and liens. A common example might leave roughly $11,167 if the case settles pre-suit at 33 1/3%, or about $8,500 if the fee is 40% after suit is filed and costs are higher.

Do all Illinois car accident lawyers charge 40%?

No. Many Illinois injury lawyers commonly charge around one-third before suit and 40% after suit is filed, but the actual fee depends on the retainer agreement. You should always read the contract closely.

Does the Illinois Health Care Services Lien Act cap medical liens?

It can cap qualifying health-care-services liens. In general, those liens cannot exceed 40% of the recovery in the aggregate, with additional allocation rules between providers and professionals.

Does the lien act mean I keep the rest of the settlement?

Not automatically. The final distribution can still depend on valid liens, unpaid balances, negotiated reductions, case costs, and other reimbursement claims.

Why is my take-home amount lower than I expected?

Because the gross settlement is not the same as the net payout. Fees, costs, and medical claims are often paid from the settlement before the client receives the final check.